- Data-Driven

- Investors

For Data-Driven Companies

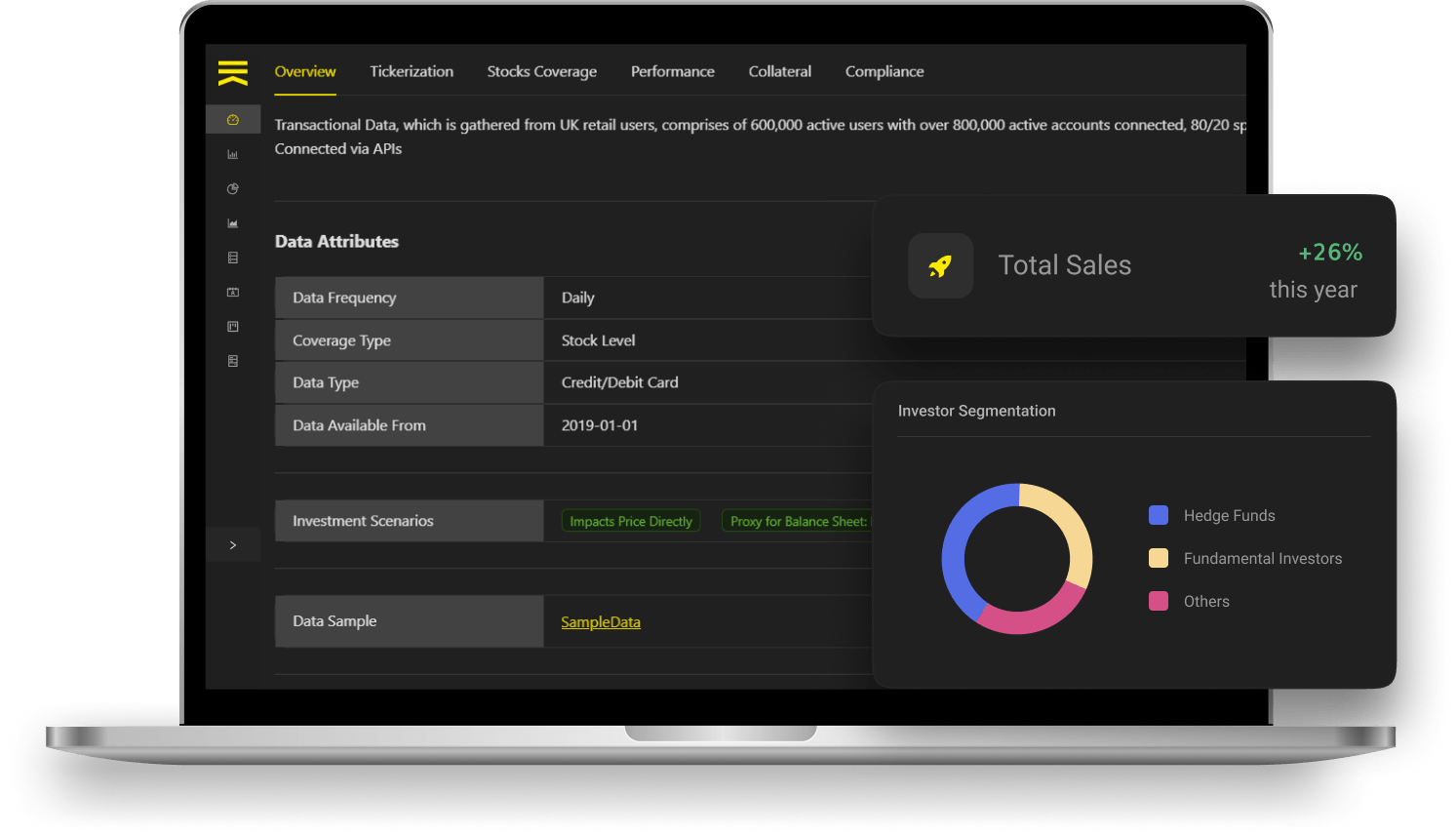

Be a Data Provider. In today’s world, every company is a data-driven organization, and with our help, you can transform that data into a valuable asset. Monetize your data with an innovative new revenue stream.

For Investors

Be a Data Buyer. A data buyer is typically an investor leveraging alternative datasets to gain unique insights. These insights from new industry data, can significantly enhance trade decisions and investment returns.